A Primer on Bonds & Yields

How bond market volatility can impact equity markets

The story of the last few weeks in finance has been the bond market volatility and its impact on equity markets.

A thread on the basics of bonds, yields, and the yield curve to help you make sense of it all...

First, a few quick definitions.

A bond is a loan given to a borrower (usually a company or government) from an investor.

The borrower is said to "issue” a bond, putting it up for sale. Investors “buy” the bond, providing the loan.

The bond has a "maturity date" on which the borrower must return the remaining principal balance to the investor.

It has a "coupon rate" - the interest rate the borrower has to pay the investor as compensation for taking the risk of loaning money.

Higher Risk = Higher Coupon.

The bond "yield" is the expected return the investor will earn by owning the bond.

The yield will increase with higher risk from:

Risk of default

Opportunity cost vs. holding something else

Expected future inflation

Bond yields are inversely correlated to bond prices.

As bond prices rise (from increased investor demand), yields go down.

As bond prices fall (from decreased investor demand), yields go up.

A primer on bonds and yields is below.

Now that we have covered the basics of bonds and yields, let's talk about the yield curve and why it matters.

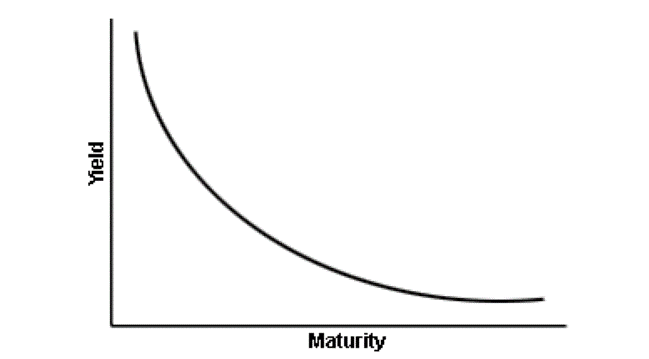

A yield curve is just a line that plots the yields of bonds with the same credit quality but different maturity dates.

The US Treasury yield curve is the most commonly discussed yield curve - the benchmark.

As the name implies, this is a line that plots the yields of US Treasury bonds (bonds issued by the US government) with maturity dates from 1 month to 30 years.

But why is it important?

The shape of (and changes in) the US Treasury yield curve can provide important information about investor sentiment in the economy.

There are four key shapes to be aware of:

Normal

Steep

Inverted

Flat

Let's quickly cover each one and what it tells us...

The Normal Yield Curve

A normal yield curve is upward sloping - yields increase with longer maturities.

In normal times, investors demand more compensation for taking a longer-term risk. There is more risk within 30 years than within 3 months!

The Steep Yield Curve

A steep yield curve is also upward sloping, but yields rise faster and higher as maturities increase.

At the start of an economic expansion, investors may demand more compensation for long-term risk if they believe rates or inflation may rise.

The Inverted Yield Curve

An inverted yield curve is downward sloping - yields decrease with longer maturities.

At the start of an economic slowdown, investors may aggressively buy longer-term bonds to lock in rates before they drop further in a recession.

The Flat Yield Curve

The flat yield curve is...flat.

It is generally viewed as a predecessor to the inverted yield curve and historically has been seen before economic slowdowns.

So now let's come back to the present.

The Treasury yield curve has been steepening dramatically in 2021.

The vaccine rollout is going well and the "return to normal" is near.

Investors are selling longer-term bonds, sending yields skyward.

But why does this matter?

Remember that bond yields are an indicator of the cost of borrowing money.

When the Fed lowers rates (as in 2020 in response to COVID-19), it is stimulative to the economy, because companies and people can borrow at low rates and put that money to productive uses.

Many companies - especially the tech darlings who were already "winners" of the pandemic - benefitted tremendously from exceptionally low rates.

They also benefitted from near-zero risk-free rates, which I talked about in the thread below.

So when the equity investor sees the bond investor selling longer bonds, there are a few implications:

The cost of borrowing money is increasing - it's now more expensive to borrow money and drive growth.

Higher risk-free rates mean more discounting of future cash flows.

As a result of this dynamic, when bond yields spiked in February and early March, the Nasdaq experienced its own sharp selloff.

Nothing had fundamentally changed about the companies themselves, but the perception of the macro situation did. This impacted their value.

Everyone looked to Fed Chair Jay Powell for assurance that they would take action to lower rates, but he was surprisingly silent.

The Fed does have additional tools at its disposal (Yield Curve Control anyone?!), but I will save that for a future thread...

So as you hear about the yield curve and its impact on equity markets, I hope this helped you feel more well-informed.

Enjoy this and want to share it with family and friends? You can find the original thread below. Subscribe now and follow me on Twitter so you never miss a thread.

Until next time, stay curious, friends!

Thank you sir, I might not fully understand the implication between the bond yields and stocks, but I have a clearer picture. Appreciate your write- up.

Perfect, needed this primer on yields, thank you